Understanding your payroll is something important because, that way, you will know, when it is delivered to you, if what they are paying you is what they owe. There are many payroll examples, but the truth is that a worker goes through many situations that make his payroll vary.

For this reason, on this occasion, we want to leave you with some payroll examples that will help you to know if your payroll and that example are really similar (changing the salary and some other amounts. Do you want to see some examples?

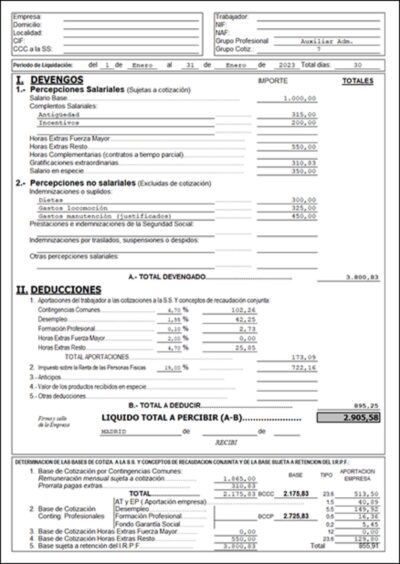

The most important parts in a payroll

Source: BBVA

We assume that you know what is a payroll, because if you have come looking for examples it is because you need to compare yours with that of a real example.

However, it is convenient that you know what the parts of a payroll are in order to know if yours is the same or is different from what should be done regularly.

So the parts are:

Payroll header

It must include the data related to the company, not only the name and fiscal address, but also its CIF number.

In addition, the worker's data will go in this part. Make sure that it not only puts your name and address, but also your ID and social security number. It also includes the start date of the worker and the job position he occupies, as well as his type of contract and the worker's qualification.

Finally, the latest data is the settlement period, that is, what that payroll corresponds to and when is the payment date.

Accruals

Here you can find two types. On the one hand, there are salary perceptions that are made up of:

- Base salary.

- Salary supplements. For example, seniority, productivity, results...

- Extraordinary hours. that go apart

- On the other hand, there would be non-salary earnings, which have the characteristic of not having a personal income tax deduction and not contributing to Social Security.

- Among them you find:

- Social Security benefits.

- Expense reimbursements.

- Compensation (for transfer, dismissal…).

Deductions

The last part of a payroll (except for the totals that come later) are for deductions, that is, what must be taken from earnings based on contributions, employee situation, etc.

In Spain, the deductions are for:

- Common contingencies.

- IRPF (if the worker advances to the Treasury part of what he thinks he will have to pay in the Income Statement).

- Unemployment.

- Training.

- Normal overtime.

- Extra hours of force majeure.

- Advances.

- Other deductions.

Total liquid perceived

This last part, always located at the bottom of the list, includes a summary of all of the above. The objective is to give the worker a net figure of what he is going to be paid for that month of work, removing the deductions that the employee has from the gross salary and all accruals.

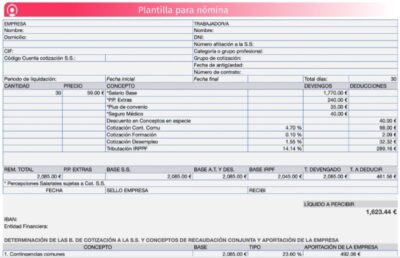

Payroll Examples

Source: BBVA

Now yes, once you understand what all the parts of a payroll are, we can leave you with some payroll examples that help you understand different situations.

Payroll of a worker with a full-time contract

Header:

Company name: FireExtreme CIF: B8281737A

Worker name: Juan Pérez

Identification number: 12345678A

Job Title: Programmer

Payment date: 01/02/2023

Payment period: January 2023

Accruals:

Gross salary: €2.000

Salary supplements: €100

Total accrued: €2.100

Deductions:

Common contingencies (4,70%): €98.70

Professional training (0,10%): €2.10

Unemployment (1,55%): €32.05

Personal Income Tax (Personal Income Tax, 15%): €315

Total deductions: €448.75

Liquid to perceive:

Total accrued: €2.100

Total deductions: €448.75

Liquid to receive: €1.651.25

Salary of a part-time worker

Header:

Worker name: Juan Pérez

Identification number: 12345678A

Job Title: Programmer

Payment date: 01/02/2023

Payment period: January 2023

Accruals:

Gross salary (part-time): €1.000

Salary supplements: €50

Total accrued: €1.050

Deductions:

Common contingencies (4,70%): €49.35

Professional training (0,10%): €1.05

Unemployment (1,55%): €16.03

Personal Income Tax (Personal Income Tax, 15%): €157.50

Total deductions: €223.93

Liquid to perceive:

Total accrued: €1.050

Total deductions: €223.93

Liquid to receive: €826.07

Payroll of a full-time worker with apportionment of extra payments

Header:

Worker name: Juan Pérez

Identification number: 12345678A

Job Title: Programmer

Payment date: 01/02/2023

Payment period: January 2023

Accruals:

Gross salary (full-time): €2.000

Salary supplements: €50

Extra pay 1 (prorated): €125

Extra pay 2 (prorated): €125

Total accrued: €2.300

Deductions:

Common contingencies (4,70%): €108.10

Professional training (0,10%): €2.30

Unemployment (1,55%): €35.65

Personal income tax (15%): €345.00

Total deductions: €491.05

Liquid to perceive:

Total accrued: €2.300

Total deductions: €491.05

Liquid to receive: €1.808.95

Payroll example of a full-time worker with payroll apportionment and wage garnishment

Header:

Worker name: Juan Pérez

Identification number: 12345678A

Job Title: Programmer

Payment date: 01/02/2023

Payment period: January 2023

Accruals:

Gross salary (full-time): €2.000

Salary supplements: €50

Extra pay 1 (prorated): €125

Extra pay 2 (prorated): €125

Total accrued: €2.300

Deductions:

Common contingencies (4,70%): €108.10

Professional training (0,10%): €2.30

Unemployment (1,55%): €35.65

Personal income tax (15%): €345.00

Seizure: €200.00

Total deductions: €791.05

Liquid to perceive:

Total accrued: €2.300

Total deductions: €791.05

Liquid to receive: €1.508.95

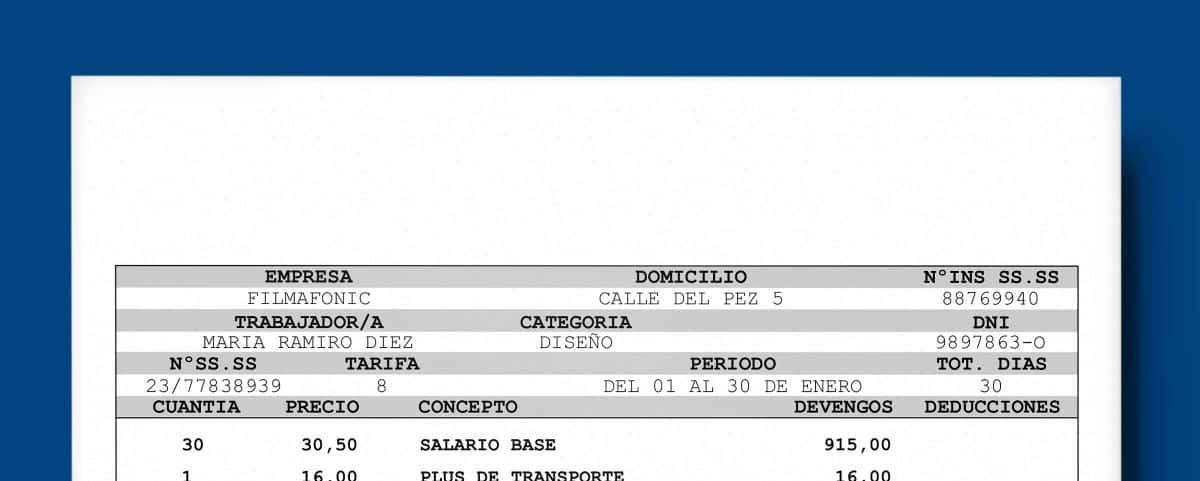

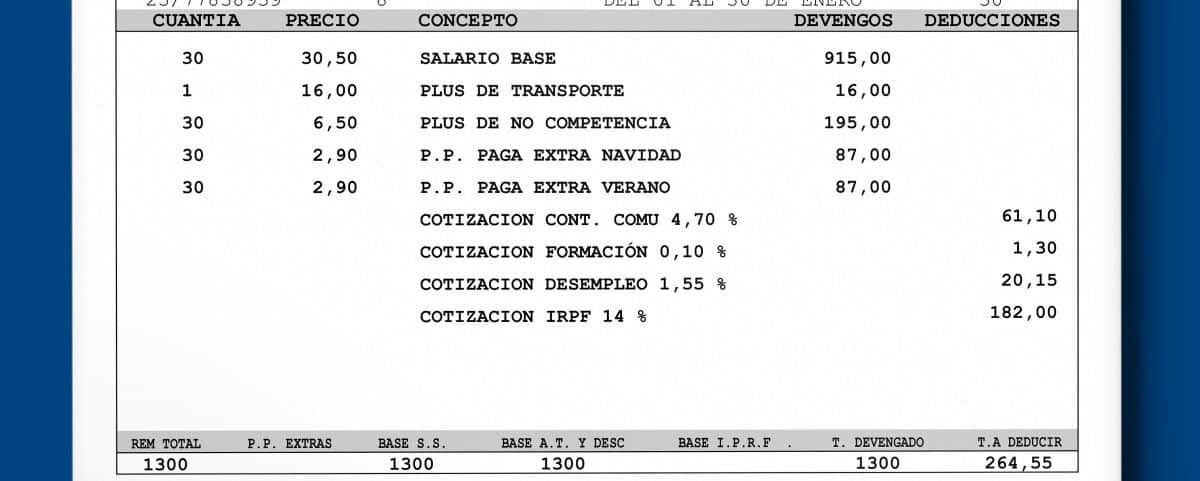

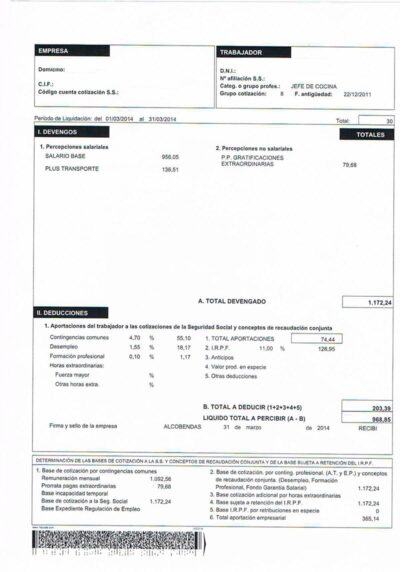

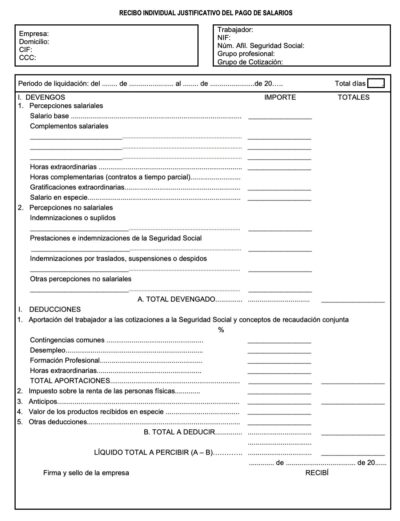

Other Visual Payroll Examples

Source: Between procedures

Source: Workers Union

Source: Templates and models

Source: Factorial

Source: Holded

As we know that sometimes, due to data like this, you may not understand it well, we have done a search to leave you with payroll examples in images so that you can see them closer to yours. Keep in mind that, although they carry the same information, the way of presenting it may differ between them since, while it contains what it should carry, the order of how it is done (or each concept is understood) may be different.

Do you have a different situation from the ones we have done payroll examples? Ask us and we'll help you make an example that can help you understand your payroll.