If you are a self-employed person or entrepreneur and your activity is subject to VAT, one of the procedures that you have to carry out several times a year is the presentation of form 303, which is known as the form of the quarterly declaration of the Tax on the Added Value (VAT).

But what is the 303 model? What people are required to submit it? For what do you use it? How should it be filled in? If you have all those questions, and some others, then we will try to answer them all.

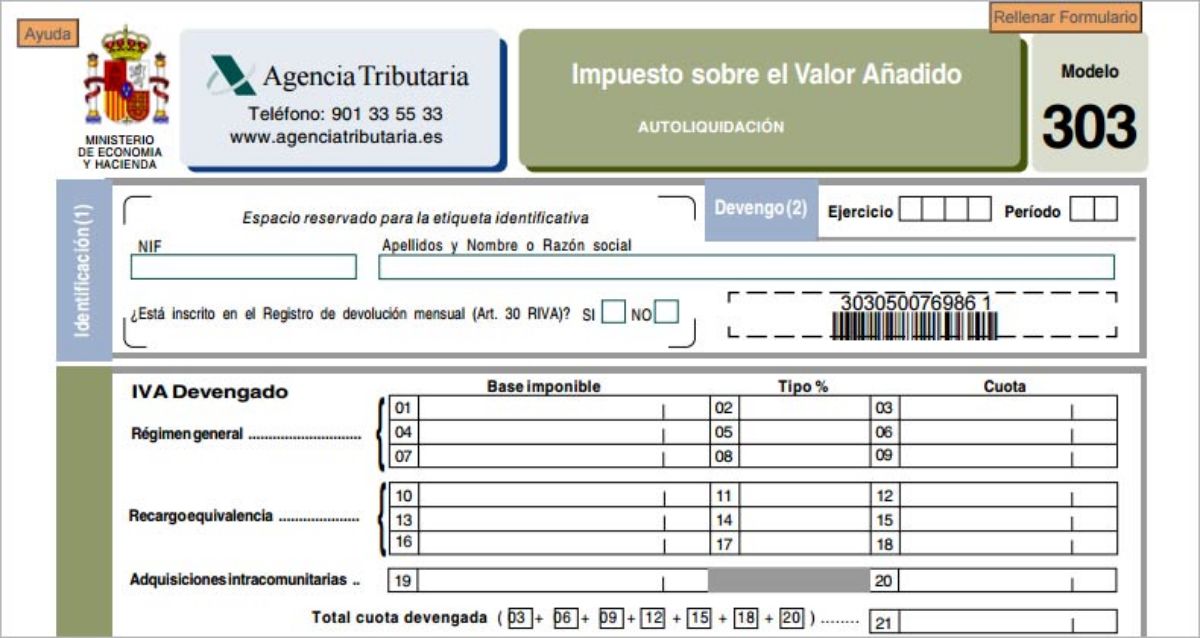

What is Model 303

Source: Cepymenews

Model 303, as we have indicated before, is the form for the VAT declaration. In other words, it is a document that reflects the VAT that you have collected, on behalf of the Treasury, through your invoices, and that now you have to enter the Treasury account.

This model is self-assessment, because in reality no one but you, who is the one who issues the invoices, knows how much you have collected each quarter and how much VAT you have collected for the Tax Agency. But you do not enter it all, but in reality you must subtract the input VAT from that VAT, or what is the same, the one that applies to you when you buy something or request the services of companies (telephone, medical insurance, etc. ).

The difference is really what you enter (if the figure comes out positive, if it comes out negative it would mean that the Treasury would give you money back).

Who should submit it

The VAT 303 model is mandatory for any professional person or entrepreneur whose activities they carry out are subject to VAT. In this case, it does not matter if it is a self-employed person, society, association, civil society ... because all of them would be obliged to do so. But are not the only ones.

Other of the groups obliged to the 303 model are the landlords of real estate or property, as well as real estate developers.

Those activities that are exempt from VAT, such as training, health, medical services, etc. They are the only cases in which they would not have the obligation to present it.

When it comes

Based on the fiscal calendar, form 303 is filed four times a year. It is a quarterly document, which covers three months, and is presented in the fourth month.

Thus, the dates to present it are:

- First trimester: it is presented from April 1 to 20. It encompasses the months of January, February and March.

- Second trimester: it is presented from July 1 to 20. Only for the months of April, May and June.

- Third trimester: it is presented from October 1 to 20. The accounts are made for July, August and September.

- Fourth quarter: occurs from January 1 to 30. In this case it would be the last three months, October, November and December.

It is important that the date does not pass, since if it happens, the Treasury can impose a penalty for delivering out of time, or even for not delivering it being obliged to do so.

Regarding the form of presentation, this can be done electronically, that is, through the Internet using the key pin, electronic ID or digital certificate (it is direct and you can pay it online as well); or by filling in the form and printing it and then going to the bank to make the presentation and payment effective (in case the result is positive) to the Treasury.

What information does the 303 contain?

Before starting to fill out form 303, it is important that you know what information you will need to be able to complete it. To do this, you need:

- The income you have had in the three-month period. Depending on which quarter you have to present, it will be a few months or others. We recommend that you break it down between the tax base and VAT, as well as personal income tax if you also apply it to invoices.

- Expenses related to economic activity. Like the income, we advise you to break it down into base and VAT, and add each amount separately.

How to fill it

When filling in the 303 form, you must bear in mind that there are two different parts.

VAT accrued

This is the VAT that you apply to your invoices when you generate one. You cannot consider that "extra" money as yours, but instead you become a collector for the Treasury and, after three months, you have to do the accounts to know how much you should pay.

There are three types of boxes here: 4%, 10%, and 21%. Most companies and freelancers pay a VAT of 21% so you would have to put in the tax base box the total of all invoices (excluding VAT) for the quarter.

The VAT accrued will automatically appear in the box next to it, which should coincide with the total VAT of all your invoices (it may vary by a few cents).

Tax-deductible

The deductible VAT refers to the fact that you have to pay for the expenses that you generate, as well as expenses of intra-community origin, investment goods and rectifications of applied deductions.

Normally in the first box you must put the base of all the expenses that you have had. Next, and without specifying if you have borne a VAT of 4, 10 or 21%, enter the total deductible VAT.

This amount is important because it will be subtracted from the previous amount of the VAT accrued.

The result of model 303 can be:

- Positive. It means that you have to pay the Treasury that amount.

- Refusal to return. In this case it is said that you have had more VAT on expenses than income, and therefore that negative amount can be returned to you.

- Negative to compensate. Some taxpayers do not want to collect from the Treasury, so they leave that amount to discount it in the following quarters.

- Zero. When VAT accrued and deductible cancel each other.

- Without activity. When there have been no invoices during that quarter.

This would be the most basic way to do the 303 model, but if you have investment goods, intra-community expenses, etc. then it can be a bit more complicated, although it will not take you long to fill in.

Once it is complete, you would only have to pay (if it is positive) and sign the document. We advise you to download the document and save it, as it is a proof of having submitted it.

As you can see, model 303 is one of the most important that you should know if you are self-employed or a company and you do not want the Treasury to put a fine on you for not presenting it. Do you have more questions about this model?