Law 1438 of 2011 allows deducting the value with which maternity leave is paid to workers who are going through a pregnancy in any of its forms.

What is the maternity deduction?

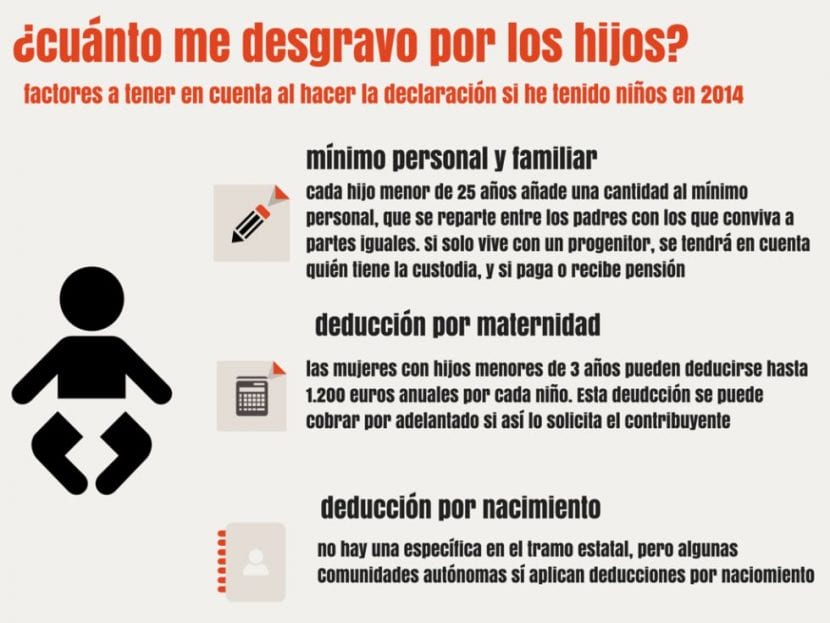

The Tax Agency mentions that the Personal Income Tax law, or IRPF, is in charge of deduct children under the age of 3 through maternity with up to 1.200 euros per year, this for each child, whether biological or adopted in Spain. Individuals who contribute to personal income tax, who have the opportunity described above, have the right to request this type of credit.

Who benefits from such a service?

This type of advance payments known as maternity deduction, are awarded by Tax Agency and they can be requested by women who have children under 3 years of age, women who in turn individually carry out activities in which they are registered within the regime that corresponds to them in the Social Security or the Mutual, this with the intention of giving a differential fee for Personal income tax of 1.200 euros per year, bonus that is given for each 3 children under 3 years of age.

In cases of adoption or foster care The voucher can be received regardless of the age of the minor, this will be respected during the first 3 years after it was registered in the civil registry, or throughout the 3 years after the date of the judicial resolution or administrative situation in which it has been declared.

If there is a case of death of the mother or in cases where full custody passes to the father or guardian, you will have the opportunity to be benefited by the bno deduction for maternity as long as the necessary requirements to acquire the benefit are met.

Income tax exemption for the benefit for maternity

The first thing we should know is that the maternity benefit It can cover a time before the birth and after the birth or before the adoption and after the adoption, and this entire period in which the benefit is being received is being taxed or a part of the benefit that is going to be paid is being withheld to property, which is the withholding of personal income tax.

Well, as is known, the State Agency of the Tax Administration or finance, does not consider that this benefit is exempt from approval, because it is not included in article 7 of the personal income tax law, which regulates the rest of the sessions as well as other series of benefits such as absolute disability are exempt. Maternity benefit is not included.

The controversy has come about the recent ruling of the superior court of justice of the community of Madrid, which says that the maternity benefit is exempt, since it makes a broad interpretation of article 7, letter H of the law of the Personal income tax; This article provides that all maternity benefits provided by the autonomous communities and municipalities are exempt from approval, however these do not include those of the State.

On the other hand, the TSJ does include that of the State, making a broad interpretation and saying that the State maternity benefit is also exempt from the IRP, therefore forcing the Treasury to return the money it has withheld from the IRP to the taxpayer. who filed the appeal.

However, the controversy grows as a result of another recent ruling from the Andalusian high court of justice, which mentions that the benefits of maternity granted by the Autonomous Communities and the Town Councils Yes, but the one provided by Social Security, that is, the one provided by the General State Administration does not. Therefore, maternity benefit, every time it comes from social security, it would not be exempt.

We find ourselves then with two judgments of two contradictory superior courts of justice and therefore it must be the supreme one through the cassation that is pronounced and says how it is interpreted, if the aforementioned is finally exempt or not. maternity benefit.

So, what happens is that until the supreme court is ruled, it may be 4 years after the mother began to receive the maternity benefit. In the event that 4 years have passed and its return has not been claimed, although the supero then says that it does correspond to the return, then it is prescribed.

In this case, if 4 years pass, it is recommended to start the administrative procedure, claim the benefit through the ordinary administrative route and then continue through the administrative jurisdiction.

In case the supreme court says no

What if the claim has finally been started and the supreme court says it would not be exempt? In this case we must be consistent and effectively stop the procedure regardless of the state it is in.

Maternity leave

We cannot stop talking about maternity leave and the legal doubts it raises.

What is maternity leave?

Maternity leave It is an economic benefit that tries to cover the loss of income or income suffered by workers when the contract is suspended or their activity is interrupted to enjoy periods of rest for maternity, adoption, foster care and guardianship. Only employed workers can take maternity leave; It is a frequent mistake to think that only these workers have the right to receive maternity leave, since this benefit is also a right of women who are self-employed, that is, the self-employed and entrepreneurs.

Another frequent doubts is if it is possible to request maternity leave before delivery. You can choose whether to wait at the time of delivery, or to request a break prior to delivery and this will be the moment when the right to receive the benefit begins. In the cases of adoption and guardianship, the right is given from the judicial resolution; in foster care cases, the right is given from the judicial administrative decision.

Apply for the maternity deduction online

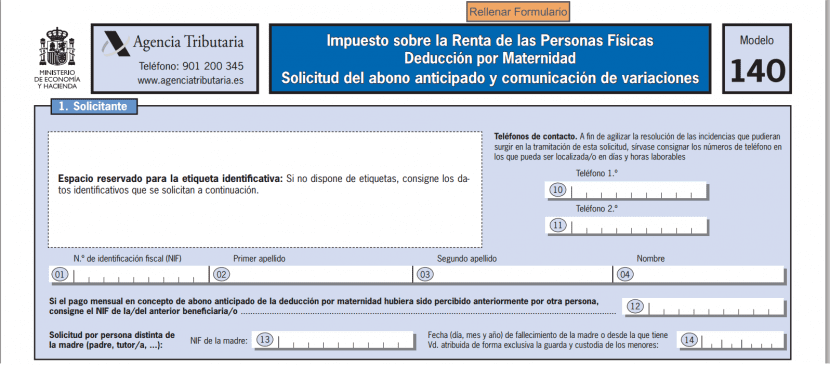

If you have the right to obtain assistance through the maternity bonuses granted by the Tax Agency, and you want to request your voucher through the internet using the web rent, below we will mention the way to do it correctly.

You must first enter the Tax Agency page. In a web account, if you want to add the maternity deduction to your file, first complete and accept the data on the identifying data screen. If you do not have to provide more data, then you will directly access the summary of returns, and later if in the section differential quota in the summary table you have the link called "Maternity deduction Amount of deduction", you can directly access the option of the declaration to include the deduction for maternity.

You can also navigate between the pages of the declaration until you find the section "Tax calculation and declaration result". To access the data entry window, press the pencil icon next to the box. Subsequently, you must access the section that says “indicate the period in which you carry out an activity on your own or someone else's account”, where you must then mark the months in which you carried out an activity.

Then indicate the contributions accrued to Social Security or Mutuality and indicate the pertinent amounts in each month quoted. Fill in all the data that appears in the following box, use the scroll bar to view all the boxes, and press accept for the data to be saved. If the changes have been saved in the correct way and you have the right to the maternity deduction, the deduction applied will be shown in the corresponding box.

To check the result of the declaration after the changes, access the window that says summary of declarations. Subsequently, locate the section of differential installment, where the incorporated deductions will appear in the list of amounts of the statement summary.

If you are satisfied with the result of the declaration, then you can press the button to continue with the declaration or save it to continue later. If no further modifications are necessary, you can file the return by choosing the mode in which you wish to present it; either joint, declarant or spouse.

What other ways can they be requested?

You can call and carry out the procedure using a bank account, a social security number, the NIF and the data from the family book.